ARTICLE STARTS BELOW

AI for Insurance: Transforming Claims, Underwriting, and Compliance

AI for insurance is no longer experimental—it's delivering measurable ROI across claims processing, underwriting, and regulatory compliance. European insurers are already achieving 50-70% straight-through processing on claims, reducing underwriting cycles from weeks to days, and cutting fraud losses by up to 30%.

At Digital Colliers, we've worked with insurance firms across the EU to implement AI systems that work seamlessly within GDPR and Solvency II frameworks. This guide explores how artificial intelligence in insurance is reshaping the entire value chain—and how to implement it responsibly.

As part of our broader AI for finance solutions, we see insurance as one of the highest-ROI verticals for intelligent automation.

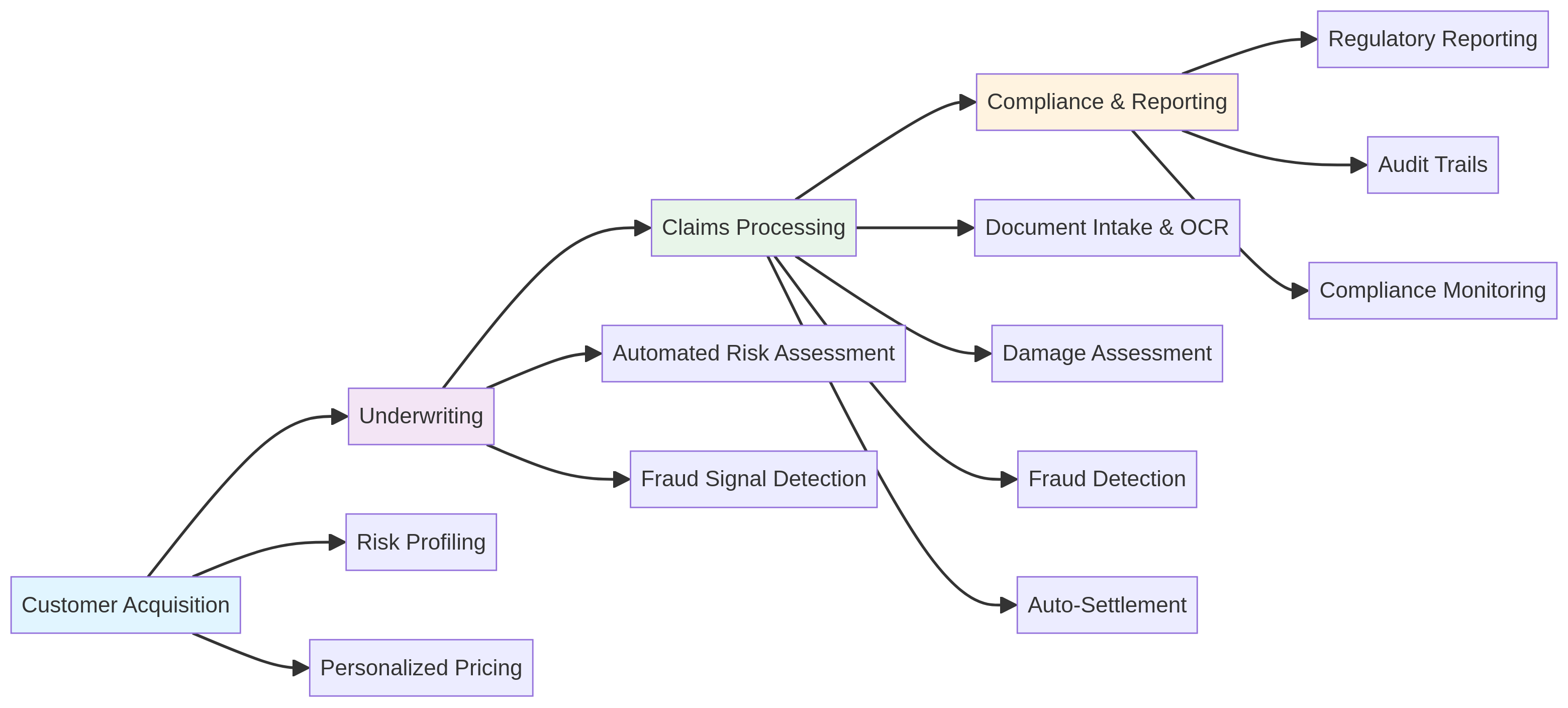

The AI-Powered Insurance Value Chain

This diagram shows where insurance AI solutions create impact at each lifecycle stage. Let's explore each:

1. Smart Risk Profiling and Pricing

AI transforms customer acquisition by building dynamic risk models in minutes rather than days.

What AI does:

- Analyzes hundreds of risk signals (claims history, behavioral data, external factors) simultaneously

- Generates personalized pricing that reflects true risk in real time

- Identifies cross-sell and upsell opportunities automatically

Real ROI:

- Insurers using AI-driven pricing see 12-18% improvement in loss ratios

- Customer acquisition cost drops 20-25% through targeted outreach

- Time-to-quote falls from 48 hours to minutes

Compliance note: All pricing decisions must remain explainable under GDPR Article 22 (automated decision-making). We ensure fairness monitoring and human review loops built into the system.

2. Underwriting Acceleration and Accuracy

This is where AI insurance solutions deliver the biggest operational lift. Traditional underwriting takes 5-14 days; AI-assisted underwriting takes hours.

How it works:

- AI pre-screens applications against policies automatically

- Flags high-risk cases for human expert review

- Learns from underwriter decisions to improve recommendations over time

- Detects fraud signals in real time (misrepresentation, policy stacking, synthetic identity)

Measured impact:

- 60-80% of applications now process automatically without human touch

- Average underwriting cycle compressed from 10 days to 1-2 days

- Fraud detection rate increases 25-35% while false positives drop

- Premium revenue per underwriter increases 40%

German insurance firm Allianz reported processing 200K+ policies monthly through automated underwriting. UK firms like Direct Line achieved similar gains within 18 months.

3. AI Claims Processing: The Biggest Transformation

Claims are where AI insurance claims technology generates the highest customer satisfaction wins. Traditionally, claims take 30-60 days. AI enables settlement in 48 hours or less.

Document Intelligence

- OCR and NLP extract data from claim forms, medical records, damage photos

- Auto-classification into claim type (motor, liability, property, health)

- Confidence scoring ensures only high-confidence extractions auto-process

Automated Damage Assessment

- Computer vision algorithms analyze photos, videos, and drone footage

- AI estimates repair costs against historical claim patterns and repair quotes

- Flags unusual patterns for adjuster review

Fraud Detection in Claims

This is critical. Claim fraud costs European insurers €11+ billion annually. AI catches:

- Staged accidents (pattern analysis + external data validation)

- Duplicate claims (across carriers, using NLP to match similar claims)

- Inflated valuations (comparing claim amounts to typical loss patterns)

- Claims filed by previously flagged individuals or networks

Straight-Through Processing (STP): Insurers report 50-70% of claims now settle automatically without human intervention—for simple, high-confidence cases. Complex cases are escalated to adjusters with AI-scored risk flags.

4. Regulatory Compliance and Risk Management

EU regulations—especially Solvency II, GDPR, and emerging PSD3 rules—require real-time reporting and auditability. AI helps.

Solvency II compliance:

- Automated capital adequacy calculations and stress testing

- Real-time reserving against actuarial models

- Predictive analysis of extreme loss scenarios

GDPR and data governance:

- AI systems generate decision logs and explanations for every underwriting/claims decision

- Audit trails capture data lineage for regulatory inspection

- Automated right-to-explanation responses for customers

Monitoring regulatory changes:

- NLP systems track regulatory updates across EU member states

- Flag policy changes that affect underwriting or claims handling

- Trigger compliance workflows automatically

Getting Started: Implementation Roadmap

Phase 1 (Months 1-3): Quick Wins

- Deploy document intelligence for claims intake (30-40% effort reduction)

- Implement fraud detection in claims processing

- Establish baseline metrics for current state

Phase 2 (Months 4-6): Underwriting Automation

- Build automated risk assessment models on historical underwriting data

- Deploy underwriting assistant with confidence scoring

- Achieve 40-50% straight-through rates

Phase 3 (Months 7-12): Full Integration

- Connect AI to pricing engine for dynamic premium adjustment

- Deploy predictive maintenance for fraud networks

- Integrate with claims and underwriting systems for closed-loop learning

Infrastructure requirements:

- Secure cloud environment (AWS, Azure, GCP with EU data residency)

- Real-time data pipeline from core systems (claims, underwriting, CRM)

- Model governance framework for compliance audits

- Change management and staff training program

Key Metrics to Track

| Metric | Baseline | Target (12 months) |

|---|---|---|

| Claims STP Rate | 15-20% | 50-70% |

| Avg Claims Settlement | 35 days | 2-3 days |

| Underwriting Cycle | 10 days | 1-2 days |

| Fraud Detection Rate | 40% | 65%+ |

| Premium Revenue/Underwriter | 100% | 140-160% |

| Customer Satisfaction (Claims) | 6.5/10 | 8.5/10 |

Challenges and How to Overcome Them

Data Quality: Most insurers have legacy claims data with inconsistent formatting. Solution: Start with recent (last 3-5 years) clean data; gradually expand as quality improves.

Model Drift: Claims patterns shift due to market changes, fraud evolution, or new product launches. Solution: Monthly retraining, continuous monitoring of prediction accuracy, automated alerts when drift exceeds thresholds.

Regulatory Uncertainty: GDPR's automated decision-making rules are still being interpreted by regulators. Solution: Build explainability into every model; maintain human review loops; document fairness testing.

Staff Adoption: Underwriters and adjusters worry about job displacement. Solution: Position AI as a tool that handles routine work, freeing experts for complex cases and customer relationships. Train staff on AI system interpretation and override procedures.

FAQs

Q: Will AI replace insurance underwriters and claims adjusters? A: No. AI handles routine, high-volume work (document classification, simple risk assessment, fraud screening). Underwriters and adjusters evolve into expert roles—evaluating complex cases, negotiating large claims, building customer relationships. Productivity increases 40-60%, not replacement.

Q: How do we ensure AI decisions are compliant with GDPR Article 22? A: All AI systems must be explainable (customers can request why their claim was denied or premium set). Maintain human oversight for decisions affecting rights. Generate automatic explanations at claim/underwriting level. We build compliance workflows into every model.

Q: What's the cost to implement AI in our claims process? A: Budget depends on complexity. Simple document intelligence: €80K-150K. Full claims + underwriting automation: €400K-800K. ROI typically appears within 12-18 months through processing cost reduction and fraud loss prevention.

Q: Can smaller insurers afford AI? A: Yes. Start small—document classification for claims. Use cloud-based models (lower infrastructure cost). Partner with an AI consultancy for implementation. Incremental rollout keeps costs manageable while validating ROI.

Q: How do we handle edge cases and escalations? A: All AI systems are confidence-scored. Claims below a confidence threshold go to human review automatically. You set the threshold—lower threshold = more automation, higher threshold = more human oversight. Build feedback loops so escalated cases improve the model.

Ready to transform your insurance operations? Contact our AI consulting team to assess your current processes and build a roadmap for claims and underwriting automation.

Digital Colliers brings 15+ years of financial services expertise and European compliance knowledge to every insurance AI project. Let's talk.